PERFORMANCE OF ISLAMIC BANKS IN AREAS OF INVESTMENT AND TRADE

NADEEM INAYAT

Conventional banking basically rests upon mobilising resources, as its major liability factor, at a predetermined rate, and primarily deploys the mobilised funds at pre-agreed interest rates. Th e linkage between savers and entrepreneurs is therefore based solely upon a fixed return, non-participatory, contractual obligation that is irrespective of the productivity of capital in the real sector of the economy. This set-up is therefore intrinsically exploitative in nature and unfair in a normative paradigm.

In the Qur’an, the charging of interest is considered an injustice and hence Riba (interest) is denounced and strictly prohibited. The Islamic laws enunciated by the Qur’an and Sunnah are the guiding principles for Islamic banking, which is an integral part of the Islamic economic system and must therefore conform to Islamic laws and should be implemented in accordance with the value system of Islam. Th e fundamental characteristic of an Islamic banking system is thus the replacement of interest by a rate of return on real activities. Th e emergence of interest-free institutions is a consequence of a growing religious spirit among Muslims.

Pioneered by Mit Ghamr Local Saving Banks established in 1963 in Egypt, there are currently 186 interest-free institutions all over the world. In order to effectively contribute to the existing study and discussion of the theory and practice of Islamic banking, this paper sets out firstly to take cognisance of the basic mechanism of operations of Islamic financial intermediaries and deduces certain assertions. Although an empirical question cannot be settled by non-empirical arguments, however the rationality of assumption and theoretical considerations so adopted imply that the Islamic bank is more yieldingly operative in areas of investment and trade. Secondly, this paper discusses and evaluates the statistical data on Islamic banks, obtained from the International Association of Islamic Banks, in terms of financial viability and deployment of funds.

This paper contains five sections. Section I focuses upon the differentiating aspects of Islamic banks and conventional banks. Section II outlines the basic working mechanism of an Islamic bank and deduces certain assertions which show the operational merit of the system based upon a variable rate of return. Section III highlights the operational results of banks using Islamic modes of financing. Section IV deals with the operational ease requirements and elaborates upon the prerequisites for the Islamic banking system to be fully operative in its true form. The concluding section summarises the findings and opens doors to further research and thought on the subject matter.

SECTION (I)

Before we examine the differentiating aspects between the Islamic banking system and the conventional banking system, it will be useful to briefly discuss Riba. Although in the past there has been dispute about whether Riba refers to interest or usury, there is now a consensus among Muslim scholars that the term Riba covers all forms of interest.

The Islamic prohibition against interest is quite clear and therefore has to be taken as axiomatic. In essence, what is forbidden in Islam is the fixed or predetermined return on financial transactions and not the uncertain rate of return such as that represented by profits.

The prohibition of interest and the fact that the banks have to rely principally on profit-sharing leads to a major difference between conventional banks and Islamic banks. The conventional bank basically links the savers and entrepreneurs through non-participatory, contractual obligations based upon fixed interest. The depositors are paid a fixed interest rate depending on maturity of deposit, whereas the borrowers are concurrently charged a fixed interest rate on the borrowed amount. The difference between interest paid to the depositors and interest earned on deployment of funds constitutes the basic earning spread of the bank. Th e money is considered as a commodity which is bought at a lower price (interest paid to depositors) and sold at a higher price (interest earned from borrowers).

On the other hand, the Islamic banking system is participatory in nature. The rate of return accrued to the savers is a direct result of the productivity of the capital employed. Viewed from a different angle, suffice to say that the savers are remunerated proportionately to the income generation of the asset portfolio of the bank, thereby making the system equity-based rather than interest-based.

If a banking structure could evolve in the manner stipulated above, whereby the return for the use of money would fluctuate according to actual profits made from such use, the resultant system would be consistent with the guidelines of Islam. This distinction also commands high merit in terms of the financial sustainability of the Islamic banking system. Under the traditional interest-based banking system, the bank lends money on a creditor and debtor relationship. In the event of loans becoming doubtful debts, the gross returns on the operating assets of the bank fall, thereby curtailing the bank’s profitability. If the bank raises interest rates (which they generally would do in such a case) to attract more deposits, or even if they retain deposits in the wake of such eventualities, the process evidently leads towards bankruptcies.

On the other hand, since in an Islamic banking system the depositor is treated as a shareholder of the bank and is not entitled to a predetermined return – rather he is entitled to a share of the profits made by the bank – the possibility of bankruptcy does not arise. Despite the uncertainty in return, the viability of the equity-based system cannot be questioned. The above distinctions by no means change the basic functioning of Islamic banks, that is, they still act as administrators of the economy’s payments system and as financial intermediaries, as in the case of the conventional system.

SECTION II

In order to fully comprehend the mechanics and operational results of the Islamic banking system, it is vital to briefly discuss the commonly used admissible modes of participation in business ventures. Aspects related to sources and uses of funds also need to be looked into in order to contemplate the quantum of savings and investment under variable rates of return.

Mudaraba

This is a form of arrangement where one of the contracting parties, called the Rab-al-mal (the financier) provides capital and acts as sleeping partner, while the other party, the Mudarib (entrepreneur), provides the entrepreneurship and management for carrying on any venture with the objective of earning profits. The net profit is to be divided between the Rab-al-mal and Mudarib in accordance with a ratio specified in the agreement. However, if losses are incurred, these shall be charged to the equity of the Rab-al-mal.

Musharaka

Under the Musharaka agreement, two or more parties enter into a contract by providing capital in different or the same amounts for running a business, with the provision that they will share in the profit or loss in agreed proportions.

Murabaha

This is the sale of goods at a price covering the purchase price plus a profit margin agreed upon by the parties. Under this arrangement, the bank buys goods wanted by the borrowers for resale to the borrowers at a higher price agreed upon by both parties.

Ijara

This is the Sharia concept of lease finance, whereby the bank purchases the assets required by the customer, and then leases these assets to the customer for a given period, the lease rentals and other terms and conditions having been agreed upon by both parties.

Sources of Funds

As in the case of conventional banks, besides their own equity. Islamic banks are dependent on the depositors’ money as a major source of funds. Under the Islamic system of banking, there are two types of deposit viz. transaction deposits and investment deposits. Islamic banks guarantee the nominal value of the deposit and pay no return on transaction deposits. Depositors can withdraw their funds at any time without notice. This type of deposit may be considered analogous to the current account in traditional banking. The other type of deposit that is available for customers is the investment deposit, which is governed by the principle of Mudaraba. In this specific arrangement, the Islamic bank will act as the Mudarib and the depositor as Rab-al mal. The bank does not guarantee the nominal value of the deposited money. Rather the depositors are treated as if they are shareholders of the bank and are entitled to a share of the profit or loss made by the bank resulting from its investment and trading activities.

Uses of Funds

Islamic banks deploy funds to shareholders in arrangements such as Mudaraba and Musharaka and transform a traditional lending activity into a sale-and-purchase arrangement under Murabaha. They otherwise arrange lease finance or Ijara. The pivotal difference between the conventional and Islamic banks on the asset side of the balance sheet lies in the nature of the role played by each bank. In fact, the Islamic bank’s first role is participatory, whereas that of a traditional bank is one of creditor and debtor. This difference in philosophy is what basically makes the Islamic banking system just and equitable and in conformity with the Sharia. The returns on the assets thus form an income stream for the bank’s profitability and consequently for depositors’ returns. Entities for funding through equity participation are therefore expected to be selected primarily on the basis of their anticipated profitability rather than upon the prime consideration of security.

In fact, cash-flow sensitivity analysis and revenue generation ability would be the effective and conclusive criteria for evaluation. Thus, under this system, there is a definite potential for:

a) greater participation in entrepreneurial activities;

b) better-yielding and more efficient projects; and

c) more varied investment projects.

These factors are most conducive not only for diversified investments but also for effective resource mobilisation and financial intermediation.

Some Assertions on Savings and Investments

In the wake of the adoption of the Islamic banking system and the introduction of the consequential uncertainty of returns, we now briefly look into the possible outcome in terms of savings and investment magnitudes. Generally, it is perceived that one of the major drawbacks of Islamic banking based upon the uncertain rate of return is the decline in savings. The question whether savings increase or decrease in an Islamic economic system is basically an empirical one. Although studies conducted do show a positive correlation between interest rates and savings, yet the study conducted by Haque and Mirakhor in 1987 concludes that there is no strong reason to believe that savings will decline as a result of introducing an Islamic banking system. Keeping this conclusion in mind, plus the fact that the trend of a positive correlation of savings with returns will be distorted by increased uncertainty, it can be asserted that Islamic banks will select yielding projects more professionally. They will also tend to diversify their lending portfolios, not only to impede the fluctuation in returns so as to give their depositors a sustainable growth in terms of profit rates, but also to reduce the possibility of potential bad debts. Both these factors would presumably be conducive to greater deposit mobilisation and further investment.

Although this causative reaction of enhanced savings and investment is an empirical question, it can be asserted that in view of the participatory role of financing, the range of production and profitability would be higher.

SECTION III

The total number of Islamic banks and financial institutions listed with the International Association of Islamic Banks is 186. The Directory of Islamic Banks and Financial Institutions – 1995 includes only 144 banks, since complete and required data on 42 banks was not available to the Association.

Geographical Dispersion

In terms of the number of Islamic banks and financial institutions, it is observed that out of a total 144 banks, 47 operate in South Asia, 24 in South East Asia, 30 in Africa, 17 in the Gulf Co-operation Council countries (GCC), 22 in the Middle East and 4 in Europe.

Summary of Financial Highlights

Although the number of Islamic banks operating in South Asian countries is the highest, i.e., 47, the aggregate paid-up-capital of the Middle East countries is the greatest, constituting 53% of the total paid-up-capital of all Islamic banks. The balance sheet footing of these banks is also highest by attaining a 59% share of the total assets of the 144 banks listed and operating worldwide.

In terms of resource mobilisation, the 22 banks operating in Middle East countries have mobilised 38% of the total deposits of Islamic banks. As a measure of financial viability, one can easily infer that region wise there is a net profitability of 53%, which is earned by GCC banks versus 29% for banks in South Asia. Concurrently, banks in the GCC countries share 36% of total reserves.

Sectoral Financing

A synoptic review of (%) sectoral financing, however, reveals as under:

Sectors Financing

Trading 29.82

Agriculture 8.53

Industry 18.92

Services 13.10

Real Estate 12.10

Others 17.13

Total 100.00%

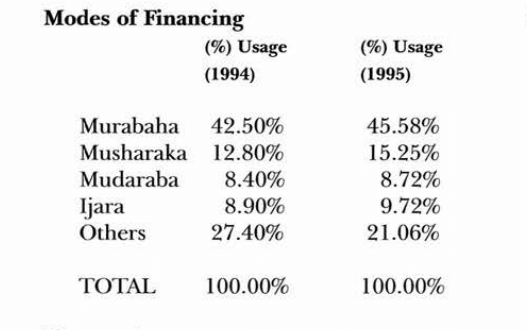

Modes of Financing

Bank-wise details of modes of financing which is as follows:

Modes of Financing

Observations

Evaluation of the data portrays that there is no doubt about the contribution of Islamic banks in the area of trade and investment and the fact that the banks are making profits indicate their financial viability. Whether these institutions are operating at optimal level or not is a matter of in-depth analysis based upon different parameters, which is outside the scope of this study. However, the modes of financing mix indicate increasing trends towards Musharaka and Mudarabah financing even within one year.

The same Directory of Islamic Banks for 1994 listed 133 banks and the percentage deployment of funds in Musharaka and Mudaraba was 21.2% of total invested resources. However, the Directory for 1995, listing 144 banks, shows about 24% of funds deployed through musharaka and mudaraba.

Further, other modes, such as mark-up, show a downward trend is an indicator of the fact that there is a growing tendency to move towards participative modes.

SECTION IV

Based upon the subject matter discussed and the data evaluated, it is now pertinent to look into the transitional issues pertaining to a total switchover to profit-and-loss-sharing based Islamic banking and to simultaneously touch upon the prerequisites of Islamic banking. There are possibly three primary reasons for the difficulties in a complete switchover to Islamic banking. These relate to inadequacy of financial infrastructure, fiscal policy objectives and legal framework.

1. Elimination of interest and eradication of false values of life is the basis on which Islamic banking rests. Honesty and fair play are the basic ingredients for Islamic banking to function effectively and successfully. Unlike the interest-based system, where the major deterrent for wilful default is the security mortgaged with the lender, in Islamic banking, it should be the fear of Allah and the people must be guided by the teachings of the Qur’an and Sunnah. Essentially, shortcomings in business ethics make it difficult for bankers to engage in participatory venture rule. For example, clients either do not keep adequate records or keep fraudulent records of their operations. Until such time that business ethics improve the banks will be reluctant to take equity positions in enterprises, as this condition is, in fact, a prerequisite for successful Islamic banking. Currently, it is also considered a pre-condition that in order to carry out detailed project appraisals and to monitor such projects, the banking personnel must have a high degree of expertise in banking and finance. The existing inability of banks to use equity-based financing is primarily due to this deficiency.

2. On the Government side, an increasing budgetary deficit is the main impeding factor for abolition of interest, especially in the absence of non-interest-based instruments for financing such deficits. In fact, a banking system not based on interest will suffer from severe limitations if it has to operate in an environment where interest continues to prevail in other major sectors of the economy. The principles of honesty and fair play equally apply to the government, which has to conduct its affairs strictly in accordance with Islamic perceptions. If inefficiency and waste were to be eliminated and people paid their dues to the Government honestly, the fiscal deficit would be minimised. In fact, problems in devising non-interest-based instruments of financing have also been responsible for the emergence of this apparent conflict between fiscal policy objectives and the Islamisation process.

3. In order to safeguard the interests of savers, banks and entrepreneurs, well-defined laws need to be enacted as per the legal requirements of the new system and the Sharia and within the ambit of a just and stable legal system. Expeditious disposal of legal cases to dispense justice to all is also required to make the Islamic banking system a success.

Based upon the above, it is quite clear why a complete switchover to profit-and-loss-sharing has not taken place. Our analysis in the previous section substantiates our above observations. Concentration on the short-term modes of financing, which are more akin to interest-based banking and require a minimum modification of the traditional banking system, is impeding the progress of Islamic banking.

Conclusion

The purpose of this paper was twofold. Firstly, to analyse the basic mechanism of operations of Islamic banks and to deduce certain eventualities pronouncing the operational merit of the system based upon a variable rate of return; and secondly, to evaluate the statistical data on Islamic banks in terms of their financial viability and deployment of funds. The basic guiding principle of Islam is Al-Adl (justice) and hence any economic activity that may digress from the principle of justice would not be consistent with Islamic values. The criterion, therefore, by which an economic system claiming to be Islamic can be measured is the extent to which Islamic principles are followed by that society.

Although concern has been expressed about the adoption of an Islamic banking system leading to a reduction of savings and restrained financial intermediation, it is, however, an empirical question and no conclusive judgement can be given. Although lending on the equity-based principle would require constant vigilance by the banks, which would imply higher-cost, professional staff, an effective and efficient judicial system, and honesty and a higher degree of morality, which serve as some of the determining prerequisites of the Islamic system, would definitely increase the yield of the real sector and consequently the rate of return. In all probability the savers would be rewarded in a real sense.

In terms of investments, the banks would be participating in ventures on operational merit rather than under security considerations. In terms of its nature, the equity-based system is non-exploitative in the sense that in the case of losses, the burden is shared. Consequently, the evil of the debt problem will not arise. The system is, in fact, more stable in terms of fluctuations and economic shocks. The system is thus quite consistent with Sharia guidelines.

Evaluation of the data depicts the contribution of Islamic banks in the areas of trade and investment and the fact that these banks are making profits indicates their financial viability. Heavy reliance on short-term financing is due to low-risk and operational ease. As discussed, there are possibly three primary reasons for the difficulties in a complete switchover to Islamic banking. These basically relate to inadequacy of financial infrastructure, fiscal policy and legal framework.

What is basically required is a total commitment to the cause, which is in complete consistency with the Divine Law. It is the faith of the Muslim that whatever is ordained by Allah is for the betterment of mankind. Hence there is no room for any reservation as to whether an economic system devoid of interest is feasible and yielding, so long as it is implemented with complete honesty and dedication.

Edited By Asma Siddiqi

Institute Of Islamic Banking And Insurance London

Comments

John Doe

23/3/2019Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat.

John Doe

23/3/2019Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat.

John Doe

23/3/2019Lorem ipsum dolor sit amet, consectetur adipisicing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat.